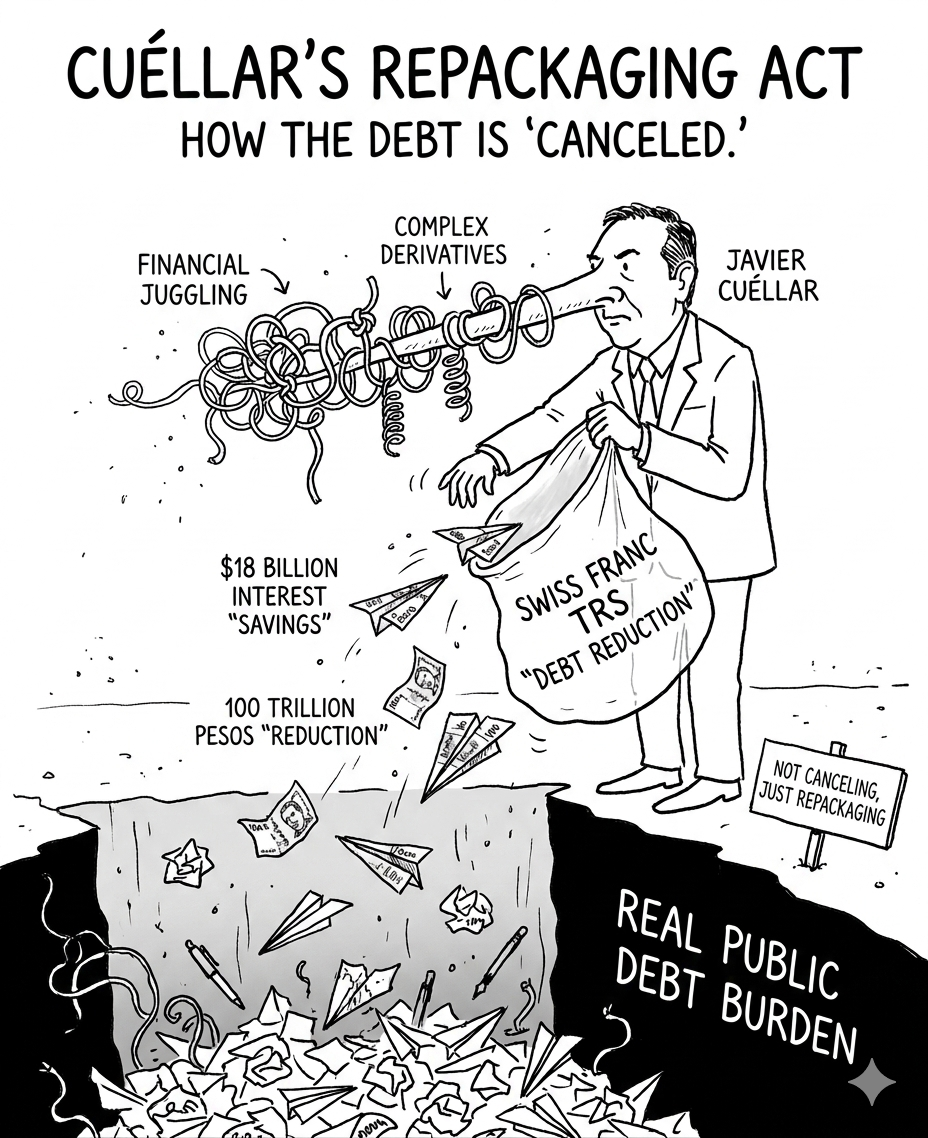

On May 19, 2026, Caracol Radio published an interview with Javier Cuéllar, Colombia’s Director of Public Credit, in which he made a series of striking claims about the government’s debt management strategy. By May 27, he said, the government will have “completely canceled” its Swiss franc-denominated Total Return Swap (TRS). He further claimed the operation has reduced Colombia’s public debt by “nearly 100 trillion pesos” and will save the country some $18 billion in future interest payments.

These are bold assertions from a government whose fiscal management has drawn criticism from economists, opposition congressmen, and watchdog agencies. But how much of what Cuéllar said stands up to scrutiny?

We investigated each of the director’s claims against publicly available data, financial definitions, and Colombia’s debt history. Here is what we found.

Claim #1: “On May 27, the government will completely cancel the Swiss franc TRS debt”

Verdict: LIKELY TRUE, but misleading.

A Total Return Swap (TRS) is, by definition, a derivative contract, not a loan. In a TRS, one party (in this case, Colombia) receives a temporary cash flow from a counterparty (six international banks) in exchange for the “total return” of a reference asset — in this case, likely Colombian government bonds (TES) or global bonds.

Cuéllar’s description — that Colombia used a TRS to raise cash at ~1.5% annual interest, used that cash to buy back its own bonds, and is now closing the position — is structurally consistent with how a TRS works.

However, the framing is important. A derivative that is being “canceled” or “closed out” is not the same as a debt being “paid off.” The TRS is a temporary financing mechanism. Closing it means Colombia returns the principal to the banks and the banks return the underlying bonds (or their cash equivalent). The gross debt position may decrease in the national statistics — Cuéllar acknowledged the operation temporarily inflated the debt figures since September 2025 — but the underlying fiscal position of the country is not necessarily improved by the same magnitude.

Claim #2: “This strategy is reducing nearly 100 trillion pesos of public debt”

Verdict: NUMERICALLY QUESTIONABLE.

Colombia’s total public debt as of late 2025 was estimated at around 55-60% of GDP. With a nominal GDP of approximately $400 billion USD (roughly 1,600 trillion Colombian pesos at current exchange rates), that puts total public debt in the range of 880-960 trillion COP.

A reduction of 100 trillion COP would represent about 10-11% of total public debt. That is a massive figure.

The problem: Cuéllar appears to be counting the gross notional value of the TRS transaction as “debt reduction.” In a TRS, the cash received is typically a fraction of the notional value of the reference assets. If the TRS was, say, a $2-3 billion equivalent operation, closing it out would not reduce the country’s overall debt stock by 100 trillion COP — it would merely unwind a temporary derivative position.

Claim #3: “The country could save approximately $18 billion in interest over the coming decades”

Verdict: POSSIBLE BUT UNVERIFIABLE, and the number raises red flags.

$18 billion USD in savings is an enormous figure — equivalent to roughly 4.5% of Colombia’s annual GDP. For context, Colombia’s total annual interest payment on its public debt was estimated at around $12-15 billion in recent years. Claiming savings that exceed one year’s total interest payments requires aggressive assumptions about interest rate spreads, exchange rate movements, and the duration of the benefit.

Claim #4: “Colombia has never entered default or payment cessation”

Verdict: TECHNICALLY TRUE for the modern era, but historically incomplete.

Cuéllar is correct that Colombia has not defaulted on its sovereign debt since at least the mid-20th century. However, this glosses over Colombia’s complicated debt history: Gran Colombia defaulted in 1826; the country defaulted again in the 1850s, 1870s, 1900 (Thousand Days’ War), and the 1930s (Great Depression). While modern Colombia has never defaulted, the statement paints a more pristine picture than history supports.

Claim #5: “The operation was done with six international banks at ~1.5% annual interest”

Verdict: PROBABLE, BUT THE REAL COST MAY BE HIGHER.

A 1.5% interest rate on a Swiss franc-denominated derivative sounds cheap — and it is, relative to Colombia’s local borrowing costs (the DTF rate was around 10% in early 2026). However, the true cost includes exchange rate risk (peso depreciation against the Swiss franc), counterparty fees, and opportunity cost on the TES bonds used as collateral. Congressman Óscar Darío Pérez called the strategy “financial juggling” and warned Colombia was “managing public debt like a casino.”

The Bigger Picture

Under the current administration, Colombia’s public debt has increased significantly. The fiscal deficit has remained elevated since the pandemic, and the country’s credit rating has been downgraded by multiple agencies. What Cuéllar described as “sophisticated financial management” looks to critics like an attempt to temporarily mask the true size of Colombia’s debt burden.

Conclusion

So — is Colombia really canceling its Swiss franc debt? The honest answer: no. It’s repackaging it.

A Total Return Swap is a derivative, not a loan. And closing one is not the same as paying off debt. What Cuéllar presented as a triumphant debt reduction is, at its core, the unwinding of a temporary financial position — one that itself inflated the country’s gross debt statistics for the past nine months.

If Cuéllar’s numbers are right, this is a clever refinancing. If they’re inflated — and the evidence suggests they are — it’s an attempt to dress up a derivative unwind as a fiscal victory. Either way, Colombian taxpayers deserve auditable, line-by-line transparency from the Ministry of Finance.